Ensure Your Dental Practice Transition Is Done Right

December 19, 2025

Key Metrics to Improve Before Selling Your Dental Practice

July 17, 2026

Written by David Haynes, MBA

The Arizona dental practice transition market remains strong, though buyers and sellers are navigating a more disciplined financial landscape than in years past. High demand driven by Arizona’s strong population and employer growth is in competition with elevated borrowing costs and rising commercial real estate overhead.

This market update breaks down the current economic factors shaping dental practice valuations and deal structures across the Grand Canyon State.

The Capital Landscape: 10-Year Treasury & Interest Rates

The cost of capital continues to act as the primary anchor for deal structures.

- The Benchmark: As of June 2025, the current U.S. 10-Year Treasury Yield is hovering around 4.5%. This sustained benchmark keeps standard practice acquisition loan rates elevated from prior years, while still in a transactable range. Most banks mark up from the 10 year treasury, and the Fed does not directly control long-term rates. When the fed changes rates, that has a much more direct impact on short-term rates, like credit cards and variable rate products.

- Impact on Buyers: While practice acquisition financing is still widely available from dental-specific lenders, the cost to borrow means buyers and banks are more focused on debt-service coverage ratios. Practices with strong historical cash flow are in higher demand because of their ability to service debt.

- Impact on Valuations: Higher interest rates have restricted runaway premiums, except in certain zip codes and situations. Practice values have held steady rather than dropping, but buyers are less willing to overpay for unproven cash flow. If we see rates continue to climb, the impact on valuation will be more pronounced.

Private vs. DSO Buyer Appetite

The competitive dynamic between individual doctors and corporate buyers remains strong, though both groups have shifted their strategies and become more selective.

| Feature | Private Buyers (Solo Practitioners) | Dental Service Organizations (DSOs) |

| Appetite Level | Extremely High. Rising build-out costs ($600k–$800k) make acquisitions much more appealing than startups. | Highly Selective. Shifted from rapid accumulation to strategic, high-margin acquisitions. |

| Target Practice | General practices with 4+ ops and revenues between $700,000 and $1.5M. | Larger, multi-doctor, or specialty hubs tracking $2M+ in revenue with strong EBITDA. |

| Deal Structure | Traditional 100% cash at closing, offering a clean, definitive exit for the seller. | Varied structures: 60% to 80% cash up front, with the remainder tied to equity rollover or earnouts. |

| Seller Transition | Short transition period (typically a few weeks to a few months). | Mandatory 3-year+ “work-back” period for the selling doctor to maintain patient continuity. |

Commercial Real Estate & Lease Rental Rates

The underlying real estate is proving to be a critical point of friction in Arizona dental sales.

- Rising Leases: Commercial lease rates in high-growth Arizona hubs—particularly across the Phoenix Metro (East Valley, Scottsdale) and Tucson are elevated. High base rents and triple net (NNN) charges compress overall practice margins. Again, this has a disproportionate effect on startups vs established practice with high, predictable cash flow.

- The Deal-Killer Risk: Buyers and lenders require the practice lease to match or exceed the length of the 10-year acquisition loan. Sellers with unrenewed leases or uncooperative landlords face significant risks.

- The Property Premium: Practices where the selling doctor also owns the real estate are commanding a premium in certain zip codes. While simultaneous property and practice sales are rare, this situation strengthen the possibility of the practice buyer owning and controlling the real estate in the future. From a sellers perspective, I cannot over emphasize working with your Menlo consultant to position your property correctly to maximize value or practice and real estate.

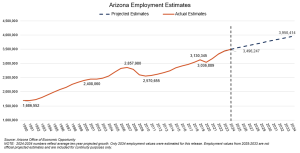

Arizona Employer Growth

As of 2026, Arizona hosts approximately 227,377 business establishments with employees, with small businesses making up 99.5% of all companies statewide. Over the past decade, the total count of employer establishments has grown steadily by about 10% to 15%, alongside a surge in overall nonfarm employment, which added over 760,000 jobs.

Within these figures, Maricopa county saw the largest employer growth in the state. Health Care and Social Assistance also saw more job growth than any other category. TSMC, Intel and other chip makers have also been huge supports to the local economy and construction ecosystem.

https://oeo.az.gov/sites/default/files/data/emp/LTIP_emp_proj_report.pdf

Summary Outlook for Sellers & Buyers

- For Sellers: Demand is robust, but preparation is key. Clean, verifiable financial records and a well-negotiated lease are essential to securing peak valuation. I cannot stress the importance of selling while the practice is stable or growing. Transacting in a decline is possible but reduces your leverage in the process

Please reach out early (even 5 + years in advance) to consult on your practice sale. Time gives opportunities to make changes that will improve your practice sale outcome.

- For Buyers: Competition for quality clinical spaces and cash flowing practices is fierce. Getting pre-approved by a dental-specific lender is vital to moving quickly when a strong cash-flowing practice hits the Arizona market. Please reach out if we can connect you with a lender. If a strong opportunity presents itself, you will want to be prepared to pounce.

{kind=link}